The year bonds weren't the safe haven

2022 was the worst year for a 60/40 portfolio since 1937. US equities lost roughly 18%. Long duration treasuries lost roughly 30%. The correlation that every TAA model built since 2008 had been exploiting, stocks falling while bonds cushion, flipped the wrong way for the first time in a generation.

The strategies that depended on that correlation did exactly what they were designed to do. GEM's 12-month momentum filter triggered a rotation to aggregate bonds (AGG) as equity momentum turned negative. Accelerating Dual Momentum (ADM) did the same, faster. Composite Dual Momentum (CDM) did the same across multiple signal windows. Paired Switching rotated between stocks and long bonds on relative strength. All of them followed their rules. All of them lost double digits.

At the same time, three strategies in a related family closed 2022 with positive returns. Not flat, not less-bad, actually up. That difference is not luck. It is the result of a specific design choice introduced by Wouter Keller and Jan Willem Keuning in 2018 and expanded on in 2022-2023, and it is worth understanding if you run any tactical allocation.

The 2022 scoreboard

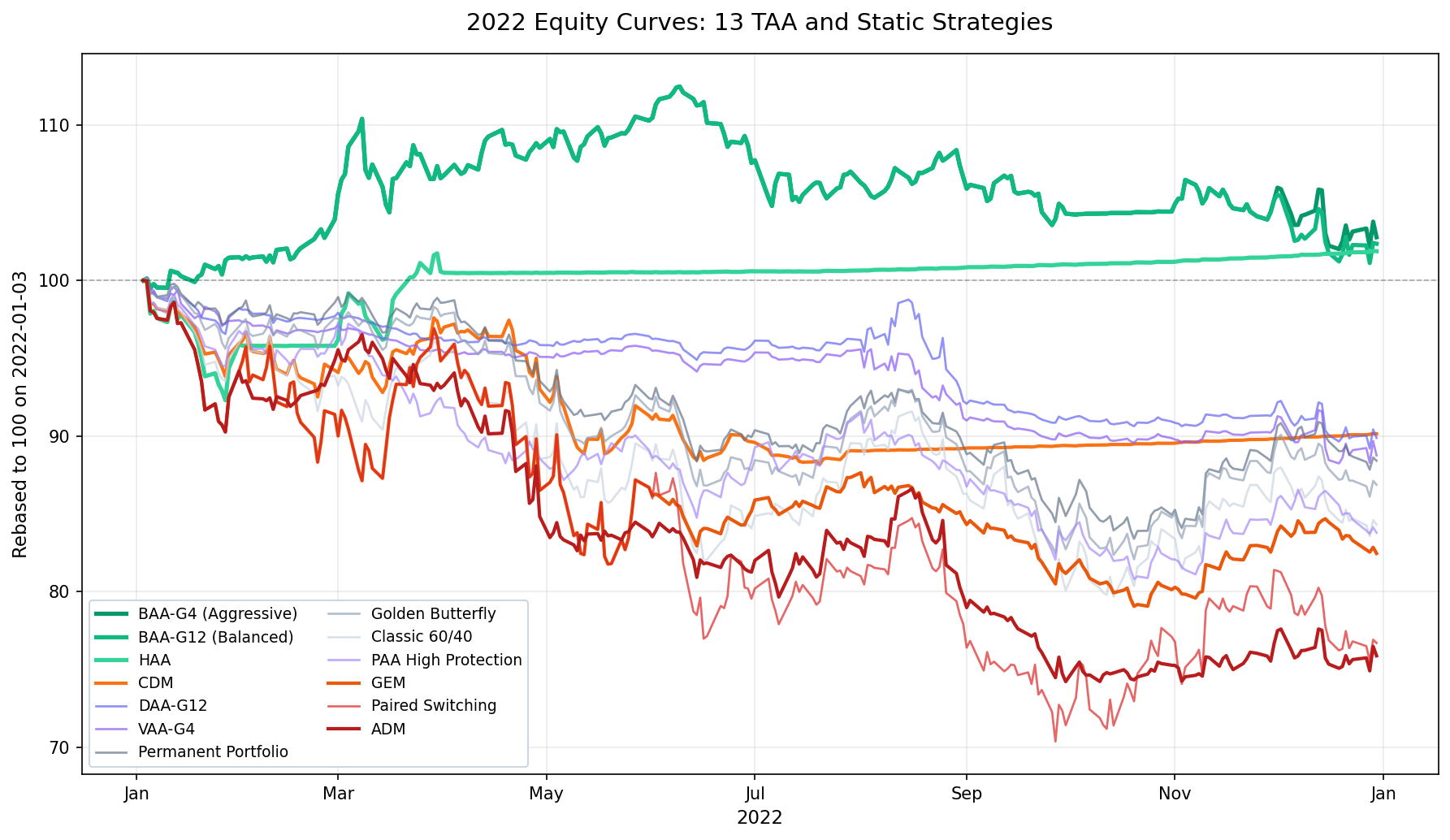

Thirteen strategies ranked by 2022 full-year return, pulled from BestFolio's production backtest database on 2026-04-21. Data window: 2022-01-03 through 2022-12-30, monthly rebalancing for tactical, annual for static, transaction costs modeled, no leverage.

| Rank | Strategy | Family | 2022 Return | 2022 Max DD |

|---|---|---|---|---|

| 🥇 | BAA-G4 (Aggressive) | Keller canary (2022) | +2.78% | -9.29% |

| 🥈 | BAA-G12 (Balanced) | Keller canary (2022) | +2.37% | -10.08% |

| 🥉 | HAA | Keller canary (2023) | +1.88% | -7.69% |

| 4 | CDM | Classic dual momentum | -9.85% | -11.81% |

| 5 | DAA-G12 | Keller canary (2018) | -10.11% | -10.97% |

| 6 | VAA-G4 | Keller (2017, pre-canary) | -11.24% | -11.83% |

| 7 | Permanent Portfolio | Static | -11.58% | -16.66% |

| 8 | Golden Butterfly | Static | -13.12% | -18.08% |

| 9 | Classic 60/40 | Static | -15.68% | -20.32% |

| 10 | PAA | Keller (2016, pre-canary) | -16.21% | -19.19% |

| 11 | GEM | Classic dual momentum | -17.53% | -20.93% |

| 12 | Paired Switching | Classic momentum | -23.28% | -29.62% |

| 13 | ADM | Classic dual momentum | -24.11% | -25.77% |

Two things jump out. The three best performers are all from the same family and all have a specific design feature. The three worst performers are all from the same family and all share a different design feature. This is not a coincidence, and it is not a story about one year of luck. It is a story about what these strategies do when their defensive signal fires.

Why classic dual momentum failed

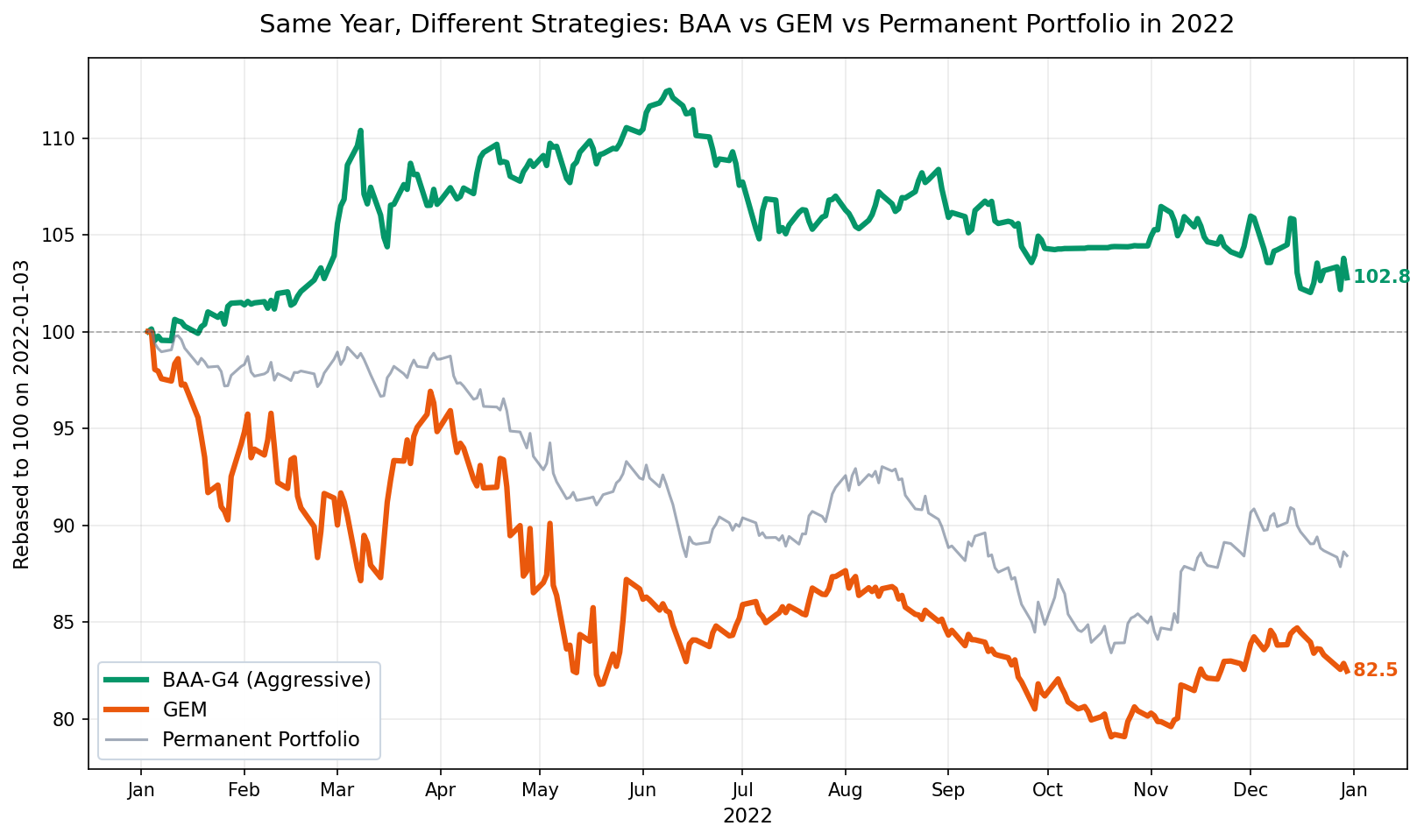

GEM is the canonical case. Gary Antonacci's 2014 formulation compares 12-month momentum of US versus international equities, holds the winner if it beat T-bills over the same window, and rotates to aggregate bonds if neither equity index cleared the hurdle. The design is elegant. The assumption is that when equities crash, bonds are the safe place to sit until momentum turns positive again.

The assumption held in 2008. It held in 2020. It held in every equity drawdown of the last thirty years we tested. It broke in 2022, because 2022 was not an equity-only drawdown. Both legs of the "stocks versus bonds" rotation were falling simultaneously. GEM's rule said rotate to AGG, AGG was down 13% for the year, and the "safe haven" was actively the worst-performing major asset class on the board. ADM and CDM faced the same scenario with the same bond-dominated defensive sleeve, and produced similar losses. Paired Switching, which rotates between stocks and long bonds specifically, walked straight into the long-duration treasury drawdown.

None of these strategies did anything wrong relative to their specification. Their specification assumed something that 2022 stopped being true.

What Keller changed in 2018

Wouter Keller and Jan Willem Keuning published "Breadth Momentum and the Canary Universe: Defensive Asset Allocation (DAA)" on SSRN in July 2018. The innovation is in the title: a separate "canary universe" that acts as an early-warning system for regime change, independent of the offensive equity momentum signal.

The mechanics, from the paper:

"The amount of cash is governed by the number of canary assets with bad (non-positive) momentum, and this strategy is called Defensive Assets Allocation (DAA)."

DAA uses two canary assets, VWO (emerging market equities) and BND (aggregate bonds). When both are showing positive 13612-weighted momentum, the portfolio runs fully offensive. When one is negative, 50% shifts to defensive. When both are negative, 100% shifts to defensive. The offensive and defensive universes are separate from the canary signal.

This decouples "what tells me to go defensive" from "what do I hold when equities fall." Classic dual momentum collapses those into one decision (if equity momentum is negative, hold bonds). The canary design asks two questions, and the "go defensive" signal can fire before the equity drawdown is obvious.

DAA in our 2022 backtest closed -10.11%, better than Permanent Portfolio, Golden Butterfly, and 60/40, but not positive. The canary fired appropriately, but the defensive universe in the original DAA specification (SHY, IEF, LQD) was not immune to the 2022 rates move. The regime signal was right. The place it moved the money was only partially right.

What Bold Asset Allocation fixed in 2022

Keller published "Relative and Absolute Momentum in Times of Rising/Low Yields: Bold Asset Allocation (BAA)" in July 2022, with an explicit framing: this is DAA adapted to a rising-yield regime. Two changes matter for our story.

First, the canary universe expanded from two assets to four (SPY, VEA, VWO, BND) with an "any negative" trigger. The slightest crack in any of the four sends the portfolio defensive. This is a faster, more sensitive alarm than DAA's two-asset breadth.

Second, and this is the one that actually shows up in the 2022 number, BAA's defensive sleeve can route to BIL (short-duration treasuries / 1-3 month bills) when longer-duration defensives are themselves falling. The paper's rule, in our implementation's docstring: "Defensive: top 3 by SMA(12) momentum; replace with BIL if asset momentum < BIL momentum." When IEF and LQD were losing and BIL was just yielding cash-equivalent returns, BAA sat in BIL.

HAA ("Dual and Canary Momentum with Rising Yields/Inflation: Hybrid Asset Allocation", Keller & Keuning 2023) does the same thing with a different canary choice: TIP (inflation-protected treasuries) as the primary regime signal, and a defensive menu that includes BIL alongside IEF. TIP's momentum fingerprint picked up the 2022 inflation shock early. BIL as an available defensive meant the portfolio had somewhere to hide.

BAA-G4 closed 2022 at +2.78%. BAA-G12 at +2.37%. HAA at +1.88%. Max drawdowns of -9.29%, -10.08%, and -7.69% respectively. Compare those drawdowns to the -20 to -30% max drawdowns the classic dual momentum strategies took in the same year. Same tactical framework, different defensive menu, and the defensive menu turned out to be the variable that mattered.

Why this isn't "Keller won"

It is tempting to tell this as "Keller strategies beat non-Keller strategies," but that is not what the data actually says. Two Keller strategies failed in 2022.

PAA ("Protective Asset Allocation", Keller & Keuning 2016) closed at -16.21%, worse than 60/40. PAA predates the canary-universe innovation and uses a "bond fraction" mechanism that rotates into IEF proportionally to the number of risky assets with negative momentum. IEF was the problem in 2022. A defensive mechanism that concentrates in IEF when equities fall is a defensive mechanism that will fail when IEF is also falling.

VAA-G4 ("Vigilant Asset Allocation", Keller & Keuning 2017, SSRN 3002624) closed at -11.24%, basically tied with Permanent Portfolio. VAA uses breadth momentum across the OFFENSIVE universe to decide defensive allocation, and its defensive menu is LQD, IEF, SHY. The breadth signal worked. The defensive assets it could choose from were all falling. VAA rotated defensive correctly and still lost money.

The strategies that had a positive 2022 are the ones whose defensive menu included a short-duration treasury option (BIL). The strategies that did not lost money in defense even when their signals fired correctly.

The real lesson is not "canary mechanic beats no canary." It is "the defensive asset you rotate to has to actually defend in the specific crisis you're rotating for." In 2022, BIL was the only major fixed-income instrument that did not lose meaningful capital. The tactical strategies that had access to BIL on the defensive side survived. The ones that only had access to longer-duration bonds did not.

Caveats we owe you

A rewrite of a previous post on this blog (Kelly Signal post-hoc correction) forced us to be more careful about implementation-fidelity claims. In that spirit:

-

Our implementations follow the cited Keller papers to the best of our reading. Each strategy file in our codebase documents the specific SSRN paper and logic it implements. For the strategies in this post, the 13612W momentum score and the canary trigger logic match the papers. The universe composition matches the default specifications in each paper. However, there are details (rebalance timing within a month, handling of dividend reinvestment on long-closed tickers, synthetic ETF proxies for dates before an ETF existed) where our implementation makes choices that the paper does not fully specify. You might get slightly different numbers at home running your own backtest.

-

One year is not a strategy test. Over 1990-2026, GEM has produced roughly 11% CAGR. BAA does not have enough out-of-sample data since its 2022 publication to make long-term claims. Everything in the Keller canary family that we discussed as a "2022 winner" has a relatively short real-world track record. The 1990-2026 long-run comparison still favors some classic dual momentum variants on CAGR alone.

-

Nothing in this post claims "2022 is the future." If the next correlation break is different, say stocks rally while cash/short bills underperform their own yield, BAA's current defensive could be the wrong choice. The rule is not "BIL always wins." The rule is "match the defensive asset to the regime you think you're facing." If you don't know what regime you're facing, a multi-asset static like Permanent Portfolio might still be your best bet.

-

Paired Switching probably deserves its own caveat. It was designed for a different problem (stocks-vs-long-bonds relative strength) and 2022 was a worst-case for its specific mechanic. Judging it by 2022 is not fair; it is in the scoreboard because we used it as a data point in an earlier post.

What to do with this

If you run GEM, ADM, CDM, or any strategy whose defensive move is "rotate to AGG or TLT when equity momentum turns," 2022 is evidence that your defense has a known failure mode. The fix is not to abandon tactical asset allocation. The fix is to add a defensive option that works when the primary defensive asset is the one falling. BIL exposure, or gold via physical/ETF, or both, solves it.

If you are new to the Keller canary family, read the papers directly. They are freely available on SSRN and the math is accessible:

- Vigilant Asset Allocation (VAA), 2017

- Defensive Asset Allocation (DAA), 2018

- Bold Asset Allocation (BAA), 2022

- Hybrid Asset Allocation (HAA), 2023

BestFolio tracks monthly signals and historical NAV for all eight Keller-family and classic-dual-momentum strategies in this post, alongside the rest of its 80+ strategy catalog. If you want to study the canary family implementations with live signals and rolling factor analysis, that is what the paid tier is for. If you prefer to read the papers and run your own backtest, that path is free and also how we think these strategies should be understood.

Bottom line

The tactical asset allocation framework is not broken. The 2010s-era implementations that assumed bonds would defend when stocks fell are broken in one specific regime (2022-style correlated drawdown), and the fix has been published and tested in the academic literature since 2018. Canary models are a legitimate design evolution, and the implementations that also solved the defensive-asset problem (BAA, HAA) posted positive returns in a year that broke every classic dual momentum strategy we track.

If you hold a TAA strategy, know which of those two problems your strategy solves. If it only has the first, the 2022 stress test is telling you something important.